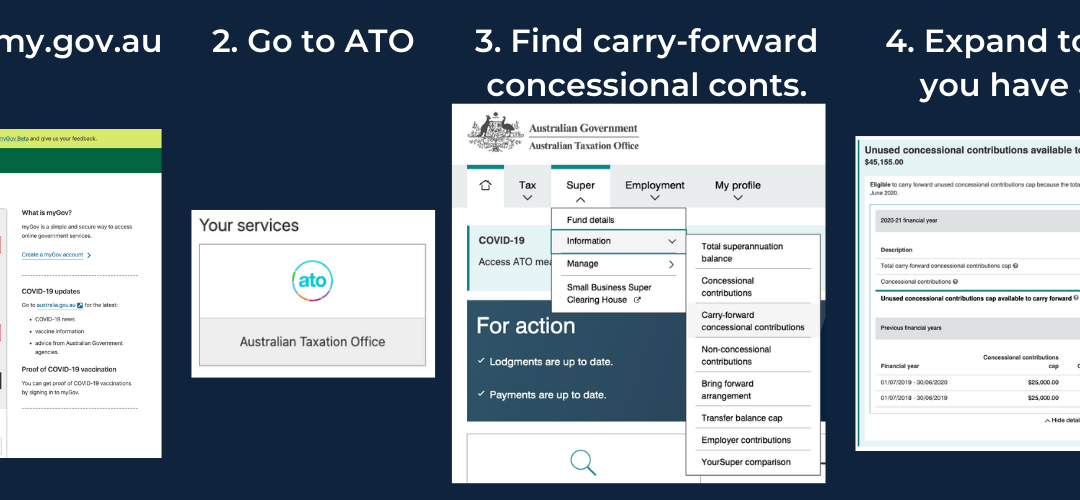

I was in studio with Geoff Hutchison for ABC Radio Drive last Friday 3 June talking about what you need to be looking at in the next few weeks regarding your superannuation. I thought a checklist might help those of you wanting to get onto the options I covered. (If...

Do you need a Self-Managed Superannuation Fund (SMSF) …or do you just WANT one? SMSF’s are an absolute boom industry in Australia. There are around 600,000 of them operating and well over a million members involved in them. So, are they a good idea?...

Oh yay I’ve got my Superannuation Annual Statement! Fran’s put together 5 Simple Steps to help you Understand and Review your Superannuation Statement: Firstly, pat yourself on the back. You’ve kept your contact details up to date and your fund knew where to...

We try to stay away from politics and religion. We are agnostic in every sense of the word in both categories. They distract from our mission of independent financial education. But we’re jumping in on an issue which is certain to impact voting in the upcoming...

By Lacey Filipich BEng(Hons) MAICD Cert Gov (NFP) When talking to people about their financial goals, a common question they seem to ask themselves (and me, and I assume their financial planner) is: How much money do I need to retire? It’s an interesting question, but...