Short answer: You may be. But have a crack at it anyway. Long answer: It’s a challenge to capture the attention of twenty-somethings when it comes to financial independence (FI). Retirement seems a loooooong way off at that age. It doesn’t matter how much I bang on...

You’ve taken Step 1 on the road to financial independence and put in place a savings plan, and next up is investments. Good work! Next you’ll need to make some choices about what to do with those precious dollars. Been watching the markets amid election pre-selection...

Do you need a Self-Managed Superannuation Fund (SMSF) …or do you just WANT one? SMSF’s are an absolute boom industry in Australia. There are around 600,000 of them operating and well over a million members involved in them. So, are they a good idea?...

We bang on about financial independence a lot at Money School. It features heavily in our blogs, and it appears in our education for kids. But what does it actually mean, and why should you care? What does financial independence mean? We define financial independence...

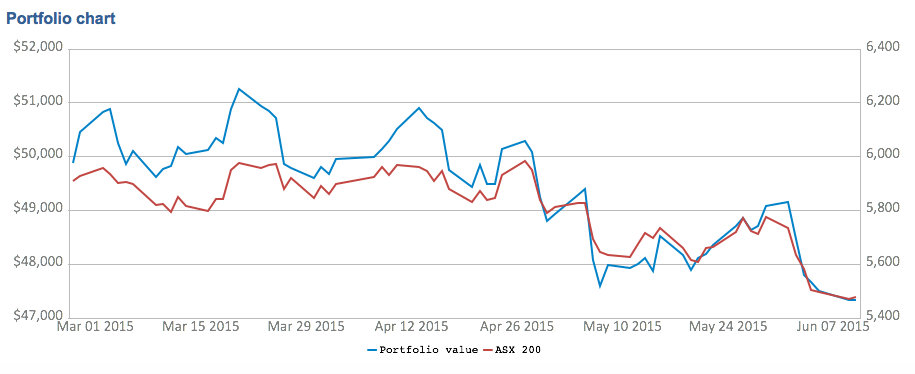

Twice a year, the Australian Stock Exchange (ASX) runs a Sharemarket Game (I’ll call it ‘The Game’ from here on in). There’s a public version for any adult and a school version for students. I’ve played it several times and I’ve sucked at it. The photo at the top of...