International Women’s Day (IWD) sends me into a funk each year. I usually feel torn between sulking, yelling and hibernating.

Why am I so angsty about this day in particular?

Because change is so slow as to make me think we don’t really want it.

Most of the root causes of the gender pay gap are systemic. We won’t see effective and widespread change until those systemic causes are addressed.

The power brokers in the places where systemic change can happen – governments and corporates – are mostly men. I remain interested mainly in what those men are doing. Yet the IWD focus remains firmly on women. Bluntly, men in powerful positions are not doing enough, and not fast enough either.

I also don’t think we’re terribly serious about making change in the corporate world.

You only need to see how many people consider International Women’s Day’s theme each year to be ‘the’ theme if it comes from internationalwomensday.com. It doesn’t. It comes from the UN Women’s Group. But we fall for the snappy hashtags and marketing of Aurora Ventures instead of doing any meaningful reading.

While we campaign and vote and protest and hashtag our way to influencing these men to change our systemic issues, life goes on. Women can still do their utmost to minimise their own personal gender pay gap.

So, in my personal contribution to closing those gaps on International Women’s Day 2022, I spoke with Geoff Hutchison and Lucie Bell on ABC Radio’s Drive program about what steps women can take.

If you’re not a woman, but you have a woman in your life: please share this article with them. The more they prosper, the better it is for everyone.

You can listen to the recording, or read on for more detail.

Note that these suggestions work for all genders and all ages. Feel free to read on even if you’re not a woman, or you’re not the age group I’m referring to.

In your 20’s: focus on being paid what you’re worth

Let’s be absolutely clear. There is a gender pay gap and a gender superannuation (retirement) gap in Australia.

The best thing you can do, knowing there’s a gap, is:

- Seek highly paid work. The highest paid jobs continue to be in the Science, Technology, Engineering and Mathematics (STEM) industries.

- Do not put up with crap. Don’t let yourself be relegated to work that’s not as ripe for promotion or advancement, as often happens to women in STEM careers. For example, I was asked to fill in as executive assistant for our site’s General Manager. Five of my male engineering graduate colleagues could have done it, but they chose me.

- If you’re a freelancer/gig worker, stay in touch with market pricing and keep pushing yours up. Especially in an inflationary environment. If you don’t put your prices up in 2022, you’re effectively taking a pay cut thanks to inflation.

- Get savvy about what a healthy relationship looks like in money terms. Joint accounts are optional. Do not let anyone take your financial independence. Learn to recognise the warning signs of financial and economic abuse. That includes control of accounts, limiting access to work and/or income, punitive spending restrictions, unequal sharing of the cost of having kids… it’s insidious. Many young women mistake it for protectiveness. Your Toolkit is my favourite resource for escaping those situations.

What if you suspect a gender pay gap in your workplace?

As of March 2022, the gender pay gap is 13.8% in Australia. This means an average woman working full time will earn 86.2% of an average man working full time over her working life.

If you suspect you’re being paid less than a male counterpart for an identical role, you need to take action because it’s illegal. The Fair Work Ombudsman can help you resolve the issue. And yes, it still happens. Late last year, I met a 15-year-old working in a pizza franchise being paid $2 per hour less than her male colleague of the same age. They were doing exactly the same work.

If you’re not on an award pay rate, it can be more difficult to know whether you’re being paid fairly. This is why pay secrecy policies are so discriminatory. But that doesn’t mean you can’t do anything.

You could:

- request the results of the gender pay audit submitted to the Workplace Gender Equality Agency (WGEA). Organisations over a certain number of employees have to submit their results each year.

- if no audit exists, ask your employer to do one. Getting multiple people in your organisation – including men – to ask for it with you can help add weight to the request.

International Women’s Day might be an opportune time to have that discussion, especially if you see your company posting lots of empowering messages on social media!

In your 30’s: think long term

This is a period when many people start a family.

They make what can become the most pivotal choice in their financial lives: the decision about how long to have off work while raising babies and kids.

Many couples fall into the trap of thinking short-term when making this decision. They weigh up the lost income of a year or two out of the workforce against the cost of paid childcare and the extra stress of having two parents working. Far too often, the discussion talks about how childcare costs come out of the lower-paid parent’s wage, and why that means it’s most cost effective for the lower-paid parent to stay home.

This is a mistake.

Childcare costs do not come out of the lower-paid parent’s wage. They’re a combined cost. They come out of the total household income. And even if you’re effectively losing money to have both parents working to some degree, it might be worth it.

See, women get a lifetime earning capacity penalty for having babies. Men don’t. That means it’s even more important for a woman to keep her qualifications up to date, her networks alive and her employability high during her parenting years.

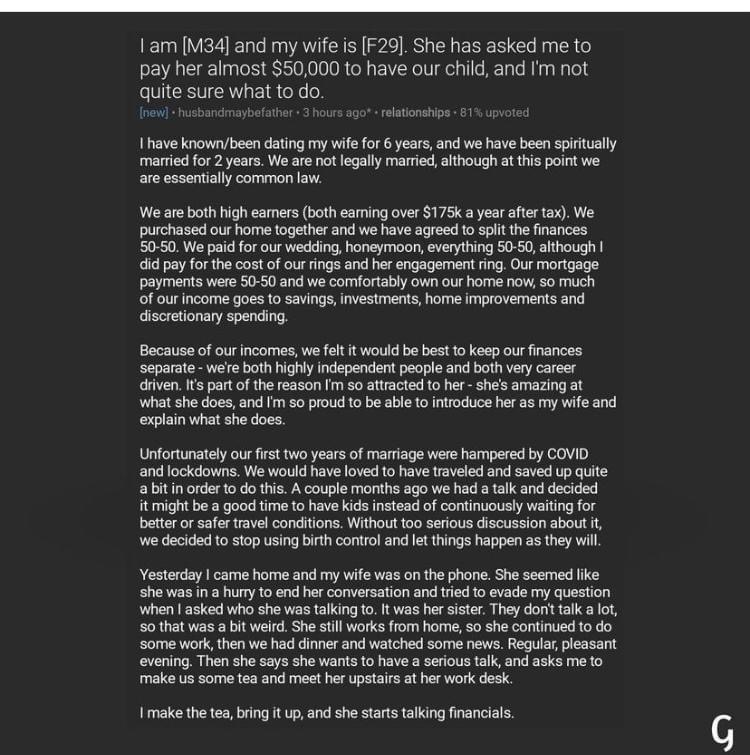

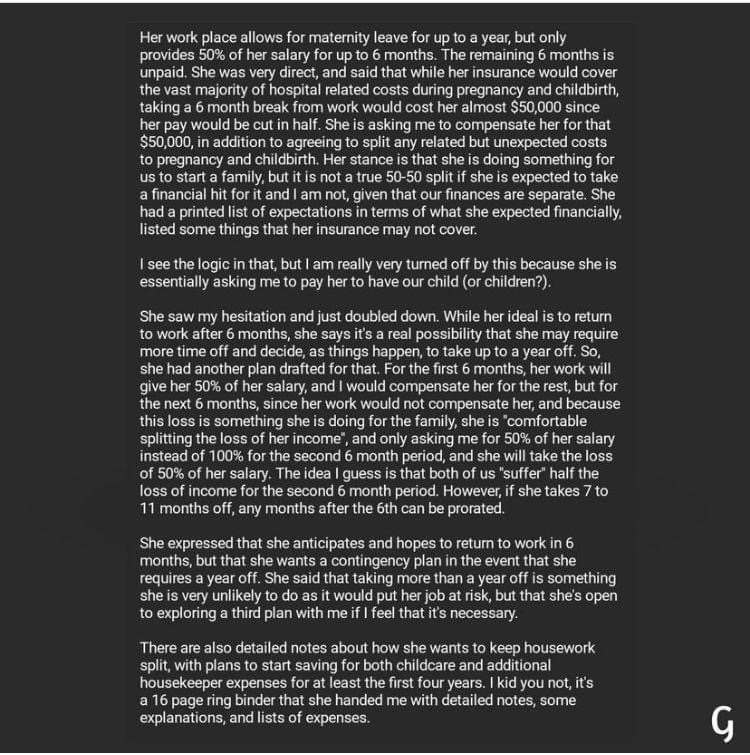

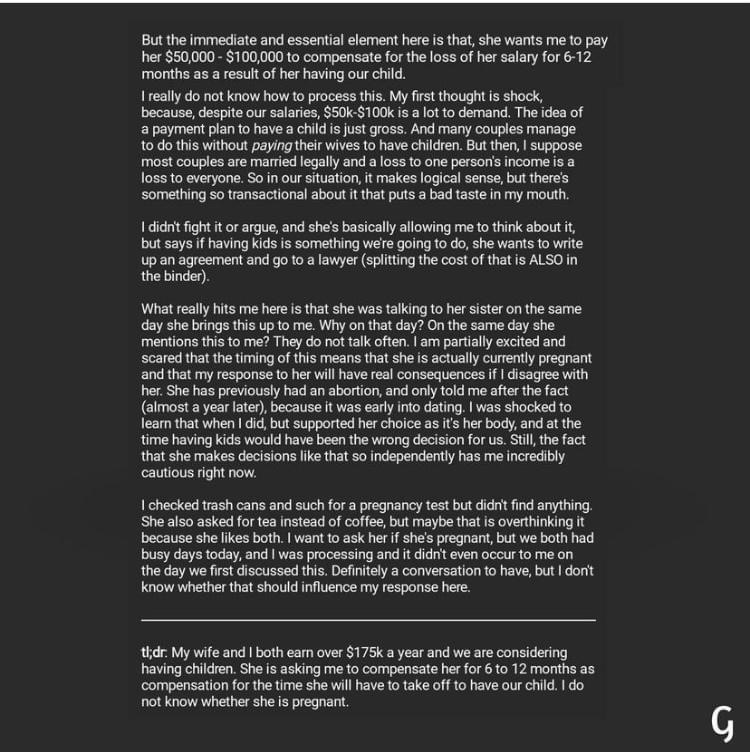

There was an excellent Reddit thread on this topic recently. A man was asking for opinions on his partner’s proposal to share the financial impact of having kids. Sadly the post was deleted. I suspect the man didn’t get the kinds of responses he was after! Here are the screenshots:

The age of women bearing the majority of the financial penalty for having kids might come to an abrupt end if this becomes common!

I’m seeing a potential theme for International Women’s Day 2023: #ShareTheBurden.

In your 40’s: get serious about your future

This is a decade when many will be raising teenagers, or they might find caring duties come into play with ageing parents.

It’s also the decade when most of my students have their first major wake-up call. Whether it’s a divorce, disease, disaster, death or redundancy, a life event often prompts them to think seriously about priorities and the time when they won’t be working anymore.

For that reason, it’s a key decade in which to ramp up your saving and investing – inside or outside retirement funds like superannuation.

You’ve still got a couple of decades before you reach retirement age, which is plenty of time to take advantage of the compounding effect.

Which is why it’s important to prioritise your financial security over your adult kids’ financial futures.

I say this specifically because I see parents debating whether to pay off their mortgage or pay their child’s HECS fees. If that’s your two options, pay off your mortgage Every. Single. Time.

You cannot pour from an empty cup. HECS is the most favourable loan your child will ever get, and their study should lead to a well-paid job. It’s much more important that you are becoming more financially secure because you have far less working life left than they do.

In your 50’s and beyond: know your rights

Empty nest divorces are common. If you find yourself in that boat: do not agree to any financial split until you’ve had advice on your entitlements. I’m heartily sick of women thinking they’re not entitled to their husband’s super when the reason he could earn that super is because you took care of the home stuff. International Women’s Day is an excellent reminder that society still doesn’t value unpaid caring work, even though it’s essential to keep the economy productive.

Even if you’re in a happy marriage, do not abdicate all financial responsibility to your partner. Many’s the case where a partner suddenly died or left, and the woman was left penniless or in debt because she had no idea what was going on financially.

Remember a binding financial agreement (BFA) can be enacted at any phase in a relationship – you can do it 30 years into your marriage, or before you get married (that’s why they’re often called pre-up).

You also need to get your affairs in order, if you haven’t already. This means:

- A signed and notarised will, ideally with legal advice so you don’t make costly and avoidable mistakes that will haunt those you leave behind.

- A binding death benefit nomination for your superannuation – kept up to date if it’s lapsing (they usually expire every three years, but you may be able to get a non-lapsing one depending on your fund).

- If you must have an SMSF, be sure to appoint trustees who will act in your best interests.

Don’t let your loved ones inherit a mess like these families did.

Finally, it’s time to get serious about how you’re going to cover your living costs when you retire.

Forget the ‘you need $1m in super’ – that’s not the case. Check out the comfortable retirement guidelines for specific amounts.

it’s also well worth looking at superannuation transition-to-retirement plans. In your mid 50’s, this can have some excellent tax advantages – get advice if you need help to interpret what’s on offer.