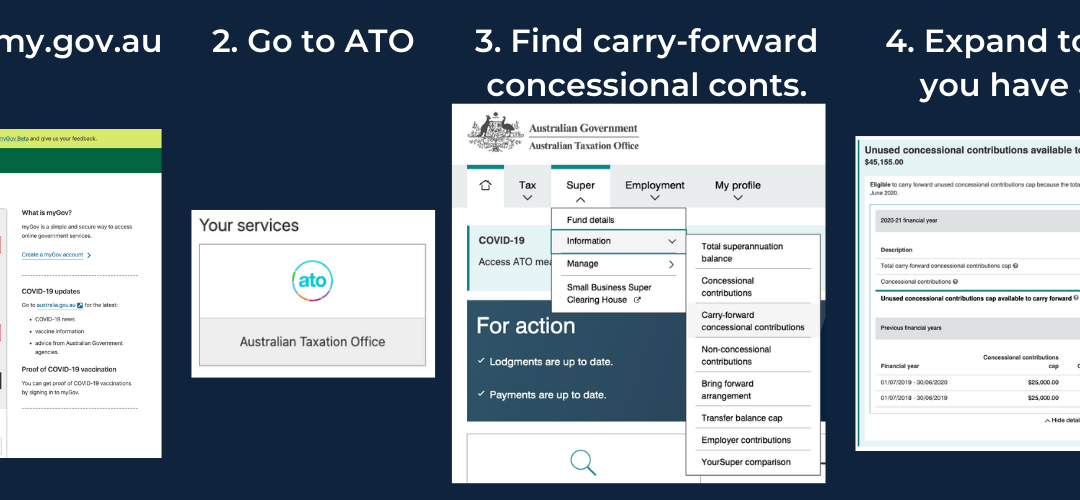

I was in studio with Geoff Hutchison for ABC Radio Drive last Friday 3 June talking about what you need to be looking at in the next few weeks regarding your superannuation. I thought a checklist might help those of you wanting to get onto the options I covered. (If...

International Women’s Day (IWD) sends me into a funk each year. I usually feel torn between sulking, yelling and hibernating. Why am I so angsty about this day in particular? Because change is so slow as to make me think we don’t really want it. Most of...

As regular readers will already know: I am not a lawyer or a financial advisor. Nothing in this article about estate management should be taken as advice. It’s for sharing experiences only. Please seek local professional help to learn how any of it applies to your...

‘Is the next big market crash coming?’ …is the questions I get most often right now. Money School readers are worried, and that’s rational. It shows you’re paying attention. Hopefully this blog helps, and the bottom line is: I’ve decided not to worry...

What official declaration of the COVID-19 pandemic means is front of mind for most of us now. For most of people reading this, it’s the first time we’ve had a pandemic experience. We’re making decisions we’ve never made before. Is it safe to go into work? Should I...