What official declaration of the COVID-19 pandemic means is front of mind for most of us now.

For most of people reading this, it’s the first time we’ve had a pandemic experience. We’re making decisions we’ve never made before.

Is it safe to go into work?

Should I cancel my holiday?

Is it a good idea to attend that function?

Should I stop catching public transport?

How much food do I need to stock at home?

Then there’s financial worries. Legitimate ones.

Immediately, there will be huge numbers of people panicking about being able to earn the income they rely on.

In the medium term, there’s flow-on effects from market upheaval. COVID-19 coupled with the oil supply flood and off the back of an already rough start to the year has smashed financial markets. There’s potential for those to hit to our individual bank accounts within the next few months.

My first instalment on this topic was triage: make a plan, build your savings, get some basic financial knowledge under your belt so you can understand the news, and look after your mental health.

Got that sorted? Now we can delve a little deeper.

So, what financial concerns has COVID-19 raised for you?

Are you worried about…

…A. INCOME DROPS?

Concerned about earning less if you have to stay home with your kids, or end up in quarantine or intensive care yourself?

With approximately one quarter of Australians on casual arrangements equating to no paid sick leave, this is a valid concern.

Apart from taking sensible precautions like social distancing to reduce your (and your family’s) chances of getting sick so you can keep working, you can:

1. Build a bigger buffer fund.

I said this in the first instalment, and I’m saying it again because I think it’s zero regrets. More savings in cash means you’ll have more to get you through a tight period of reduced income.

If it turns out you don’t need it – wonderful! You’ll have some savings to deploy to whatever you choose in the future, be that paying down debt or investing or a well-earned holiday.

If you do need it, you’ll be glad you made the effort to save ahead of time.

The time to save hard is before your income takes a hit. You probably don’t know when that will be. So, do some temporary belt-tightening now to get ahead – if you can.

2. Check your income protection insurance.

If you rely on your wages, and especially if you’re living month-to-month, you may have income protection insurance.

If you don’t have it already, maybe having some will make you feel less stressed, but it probably won’t help you this time round if you don’t have it already.

BUT FIRST: Make sure you check the fine print on any new or existing policy. Would pandemic quarantine qualify you for payment? Or do you have to contract the disease before your insurance would kick in? Or is it not covered at all? Each policy is different, so you need to check yours carefully.

Find out now so you can rest easier.

Side note: Perhaps you’re pissed about other insurance that’s void due to COVID-19 being declared pandemic – for example, travel insurance. As my insurance broker buddy reminded me last night, there’s probably not enough cash to reimburse everyone if insurance companies had to pay out on everything that will be lost this time around. This article in the New York Times on business continuity insurance is an interesting one.

3. Take it online.

There are millions in jobs that require a physical presence – for the time being at least. Transport truck drivers, medical professions like paramedics, nurses and doctors, carers for our elderly, builders, plumbers, childcare workers… the list is long.

But: some work can be done remotely. Likely a lot more than is done right now.

Even if just 20% of your role could be done out of the office, this seems like the time to give it a shot!

(Side note: I’ve never been so glad to have a mostly online business as I am right now.)

4. Contingency planning for caring

If you’re a parent, or if you have loved ones in their 60’s or older, you might soon find yourself having to care for them on a full-time basis if you’re not already.

This could be due a child’s school or daycare closing. Perhaps your partner will need help. It might be a parent who gets COVID-19 but isn’t sick enough to need a precious intensive care bed. That’s a much better problem than them needing the bed of course! But it will still require some planning.

Knowing this might be coming, have a plan on how you’ll cope.

Will you ask family members to step in if your kids are home for school closure but not unwell? It’s a tough call with COVID-19 hitting older people harder on average.

Will you look for a paid option like in-home care, babysitting or a nanny for a short period, assuming you can afford and find one?

Will you make arrangements with neighbours or friends to share the caring load so you can still manage some work?

Think ahead so you can put the plan into action if needed, and don’t have to scramble to make a plan if it does happen.

…B. STOCKPILING FOR QUARANTINE?

It’s been the subject of much meme-related hilarity this last fortnight. You may be laughing, but please exercise some compassion too. Hoarding basic supplies is a normal coping response to fear of lockdown. These people are fearful, and yes it may be making them a bit foolish.

We’ve been told supply chain interruptions of two to four weeks are possible, and that we should have a month’s prescription medication on hand in case that comes about.

It’s led to empty shelves and stressed-out shoppers.

What worries a lot of people (including me) is those who couldn’t afford to buy in bulk, or couldn’t get to the shops promptly because they were waiting for social security payments or help.

By taking more than you really need, you’re making it harder on people with fewer resources than you. This can be catastrophic for them in the short term, leading to hunger and poor health.

Which means it’ll eventually hurt you too, as they load up the health care system. So don’t think ‘well, that’s their problem.’ It becomes yours too, eventually.

We have to find the balance between enough to get through and hoarding.

For our own wellbeing and for those of our fellow citizens, you can:

5. Buy things you already eat and use.

Just because kidney beans have a great shelf life doesn’t mean you have to buy them if you wouldn’t normally. We’re talking about lasting through two to four weeks people, not to the end of the decade.

Best bet is to get a few cook-ups ahead on ingredients for tried-and-true recipes you know you’ll eat. Bonus points if you can freeze cooked portions for consumption later so you aren’t throwing away leftovers.

Otherwise you end up with a pantry full of stuff you’ll still be looking at in 12 months time, wondering what to do with it. It’s a waste for you, and it’s putting pressure on those who can least afford it because they’ll have to hunt – and pay premium prices – for basics.

I have three cans of tinned beetroot staring at me accusingly every time I rummage in the back of the pantry, so I speak from experience with this one. #Buyersremorse.

6. Be realistic about what you’ll use in 2-4 weeks.

It’s tempting to go for more than you think you’ll need. But think twice – there’s no need to be wasteful, and not just financially.

Here’s an example you might use to work out what you need: Hubby and I already spend a lot of time at home, and we use around three rolls a week. If our two kids end up at home during weekdays due to school/kindy closing, we might use one more. Four rolls a week equals eight to 16 rolls in the period we’ve been told to expect shortages.

Sidenote: How do I know it’s three rolls usually? No, I don’t count. We get 3x 48-roll deliveries a year from ‘Who Gives A Crap’, so I calculated 48 rolls x 3 deliveries / 52 weeks = ~3 rolls a week. If the kids end up at home instead of school, it might go up another roll. My latest delivery came the week prior to #toiletpapergate, so I’m well and truly stocked up.

How about your food stocks? I looked in my pantry. I reckon I’ve got a couple months of food in there, and that’s nothing unusual for most families on average or better incomes in Australia.

If there is a supply interruption, I’m going to treat it as a challenge to clear out the stuff I haven’t used. Maybe you can too? Those beetroot cans’ days are numbered.

7. Put a date in your calendar to give what you don’t use away.

If you have already gone a bit overboard on the hoarding, don’t beat yourself up too much. Thank your survival instincts for looking out for you.

Then make the sensible part of your brain take over.

Make a date in your calendar to give away what you didn’t use before it expires. Christmas might seem far away, but it’s a common time for food drives. Be ready to part with those unused basics if it turns out you don’t need them.

Keep an ear and eye out for family, friends and neighbours who are short on something. Can you help them out? #Sharingiscaring.

…C. STEMMING YOUR LOSSES?

Whether you’re looking at the value of your superannuation or assets you hold outside of your retirement fund, you’d have to be stoic to watch a 25% shedding and not react.

It would be particularly tough for someone relying on income from their superannuation fund.

First, remember that reduced share prices don’t always immediately translate to reduced dividends. So, your income may not take a big a hit as you’re thinking based on share prices in the short term.

Next, you can:

8. Change your investment mix.

You can change your investment mix within your superannuation.

If you’ve seen a lot of value loss, you could consider switching to something that would be ‘safer’ – like a conservative mix heavy on cash and bonds.

Of course, the best time to do this was last week. But if you think falls may continue, perhaps you’ll rest easier if you make the switch.

Check with your fund first, but it should be free to do this once a month. If it’s not, give them a call – it’s supposed to be policy!

You can do this outside of your superannuation too, if you’re willing to take the loss. If you’ve got plenty of time before retirement up your sleeve, you’d want to think long and hard before you exit if you haven’t already.

…D. GRABBING A BARGAIN?

There’s definitely blood running in the streets right now.

Alan Joyce not taking a salary for the rest of the financial year is one example of the lengths companies will go to so they can scrape through these conditions without going belly up.

The market may get worse – or it may not.

If you’ve got excess cash burning a hole in your pocket and you’d like to grab a bargain in the shares fire sale:

9. First: get practice if you’re new

Although tempting, during a pandemic seems like a risky period to try share trading for the first time. If you’re a newbie, you might like to consider putting your training wheels on first.

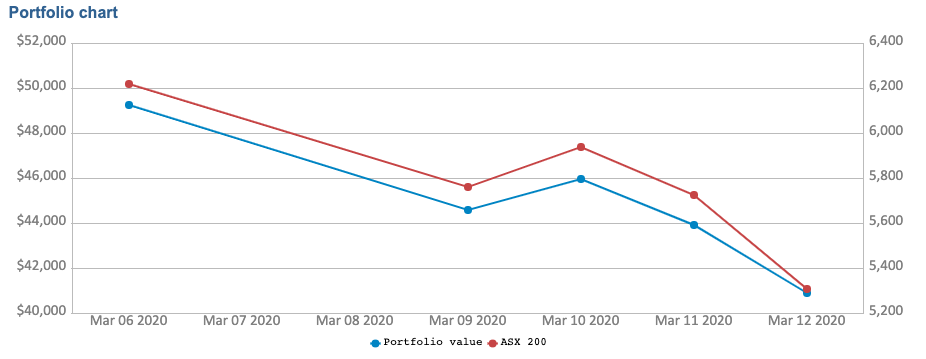

Personally I like the ASX Sharemarket Game, which gives you a virtual $50k to trade in a live market.

Try it out first. Then see if how you feel if your portfolio looks like this a week in:

Yep, that’s my portfolio in the ASX Game now.

You may find it’s not fun. In which case, you can think twice before putting actual cash on the line.

You can also pick a strategy to try. Feel free to join the ‘Money School L Plates’ league if you want to do it with friends (ID 28988, password buffettordalio). Here are some options:

10. Long haul? Decide when you’ll buy.

If you’re buying for keeps – for example, you’re after index funds like Vanguard that you plan to hold for decades – this is the single most important decision you need to make.

Are you going to try to buy while shares are dropping, or will you wait for a turning point?

Keep in mind that turning point may be days, weeks, or months away. Maybe even years if this goes critical and our financial system ends up on life support.

Timing the market so you buy at the exact bottom is nigh impossible.

If you accept that, there’s two common approaches. See which resonates with you:

Buying on the way down

If you want to buy small parcels of shares frequently, you’ll probably look at dollar cost averaging. It means you average the price you pay for a given share over the purchases you make.

If you’re buying small amounts on the way down, this approach means you get more shares for the same amount of money each time you buy.

Which means you might be buying shares this month.

Waiting till the market turns

Some of us can’t resist waiting for a bargain (this is me). We’d rather wait till the market is showing signs of improvement before we buy.

This might mean you wait for months or years before you purchase. You might wait for positive economic indicators like new building approvals and inflation to turn around.

If this is you, you’ll want to think about what would give you enough comfort to buy. Have this planned in advance. Otherwise, you may find yourself waiting too long to capitalize on the discounts available.

11. Fortuneteller? Picking companies that will fare well in this environment.

Because of all the carbohydrate rich food being hoarded, there’s been suggestions that shares in companies producing laxatives might be smart.

I saw Paul Benson mention Zoom’s share price rising in his newsletter. They’re a videoconferencing company, so that make sense with more remote work happening.

Producers of hand sanitizer and soap are probably also in a great position to capitalize on this catastrophe. Home improvement suppliers that deliver might thrive while we’re all locked in our homes. I confess I thought about buying 20L of wall paint this week, just in case. Then I came to my senses.

What other companies can you think of that will fare well in a pandemic?

You might be tempted to pick shares in those companies, hoping to see a quick rise in share price, or perhaps you’re hoping for a sustained boost.

If you go this way, remember that active trading is a job – you have to put time into learning how to do it, and then you have to do it.

12. Opportunist? Picking companies at heavy discounts.

I’m seeing a lot of people commenting on buying airline and cruise company shares ASAP. They’re looking at share prices that have taken a hammering and hoping to see that turn around.

It’s a vote for capitalism and recovery, and for that company’s resilience, and for its industry’s longevity.

I can’t see humans never flying again, or never cruising again. But as to picking the winners? I don’t want to do the analysis right now. But perhaps you do?

…E. WHAT TO DO IF YOU’RE QUARANTINED?

Two weeks cooped up at home might seem like your worst nightmare.

If you’re sick, you’ll probably be resting and trying to recuperate.

If you’re not sick – as in you’re self-quarantined due to risk factors, or you’re looking after yourself – there’s only so much cleaning, cooking and Netflix you can take.

You could:

13. Reduce your costs

Stuck at home with internet and a computer? Here’s your golden opportunity to cut waste from your day-to-day spending. Even better, you can enlist any children at home old enough to drive Google to help you.

Download your bank and card transactions for the last year for a spending audit. What’s been unusual? What could be cancelled? Knowing what you’ve spent means you can make changes to the areas of greatest impact. #Dataisyourfriend.

You can shop around for alternative suppliers of power, gas, insurance and the like. Get them on the phone and hone your negotiating skills. Ask your bank for a mortgage rate reduction. Yes, an even bigger one than the RBA just gave you.

You might not make money while you’re at home, but at least if you’re saving money you’re not as far in the hole.

14. Get your house in order

…and I don’t mean cleaning out the pantry.

This is a great time to check:

Your insurance is adequate. You know what you’re entitled to. You have your documents on hand – including policy numbers and the product disclosure statement (PDS) so you can access them if needed.

Your will is up to date. It’s covering your existing family arrangements. It has been written correctly, notarized and is lodged properly.

Your enduring power of attorney is in place. It allows someone you trust to make health and financial decisions on your behalf if you are incapacitated, e.g. you end up in a coma. It has been written correctly, notarized and is lodged properly.

Your binding financial agreement (BFA) with your partner is in place, if you want one. You can create this document at any time – it doesn’t have to be prenuptial. It’s also optional.

Are all your docs stored appropriately, with electronic and paper back up? Get the kids operating the scanner if not.

15. Treat it like a mini-retirement.

It might not be the one you’d choose, but home quarantine (if you’re not unwell or caring for someone else full-time) could be your first mini-retirement!

What would you do with two weeks off? Like, really off, with no travel or family commitments?

Yes, you’re confined to home, but there’s so much you can do from home these days:

- Been dreaming of learning a language? Here’s your chance.

- Always wanted to learn about money? Take a course. (We’ve got one you might like…)

- Suffering from tsundoku? Catch-up time is here.

- Desperate to learn to code, or build a website, or start a business? Batter up.

I’m a huge fan of edX for free courses, and I’ve got a backlog of paid courses I bought but didn’t complete. You can guess what I’ll be doing if quarantine happens.

*

That’s a big laundry list of stuff. Pick and choose what you will.

I hope you find it comforting, even helpful, in stressful times.

Thanks for this. Self funded retirees here, drawing pension from super. Not eligible for Centrelink. Checked super balance last night and heart nearly stopped. Stoic? Nope. But not going to pieces. At least we have loo paper for a few weeks.

Oh man, I can imagine the shock! The stockmarket has not been pretty. Glad to hear you’re not going to pieces though Leah 🙂

Hey I have the perfect recipe for your tinned beetroot. https://www.bestrecipes.com.au/recipes/beetroot-chocolate-cake-recipe/3zpjdu8g

I too am suffering from tsundoku, but if kids are home, am unsure I’ll get extra time!

Otherwise some really great suggestions for things to do with your time (my scanner is going to get a workout!).

Nyssa! You champion! I am so excited about that recipe. Farewell beetroot 🙂

Great to hear you liked the tips! I hope it’ll feel good, getting that personal admin stuff done.

I love this list! I am super keen to have a go at the sharemarket game – kicking myself for not being more interested in it when my younger brother was doing it at high school!